China’s Stock Rally Anticipated to Decelerate as AI Investment Reaches Saturation, Survey Indicates

Experts indicate that Chinese stocks may experience a slowdown in momentum as the year closes, with valuations becoming increasingly stretched. This situation raises concerns about whether advancements in AI and supportive policies can foster a lasting market recovery.

The CSI 300 Index is expected to end the year near 4,675 points, according to the median forecast from 16 analysts and investment managers surveyed by Bloomberg. This suggests a modest increase of 1.2% from Monday’s closing value, following a year-to-date surge of 17%. Projections for 2026 remain cautious, with only a 5.5% rise anticipated by the end of next June, according to an informal poll conducted from September 18 to 24.

The survey results underscore a cautious outlook; while China’s “uninvestable” status has eased, significant concerns persist. Geopolitical tensions, unpredictable Trump-era policies, and a slowing economy continue to deter major capital from the market, even amid AI-driven trading and a temporary truce with the U.S. regarding tariffs.

“The priority for 2025 will be maintaining stability,” stated Haris Khurshid, chief investment officer at Karobaar Capital, one of the survey participants. “Although policy support exists, it is inconsistent, and global investors are reluctant to assume more risk until geopolitical strife calms down.”

Respondents also anticipate the Hang Seng Index to rise by approximately 2% by year-end compared to current levels.

ADVERTISEMENT

CONTINUE READING BELOW

‘Crowded’ AI Trade

This year’s extraordinary rally in China has been primarily fueled by enthusiasm surrounding AI-related sectors and technology. The Hang Seng Tech Index has soared by 42%, mainly driven by domestic chipmakers like Hua Hong Semiconductor Ltd. and Semiconductor Manufacturing International Corp., which have seen increases of over 233% and 140%, respectively. Alibaba Group Holding Ltd. witnessed a nearly 50% rise in September as it unveiled significant AI funding initiatives.

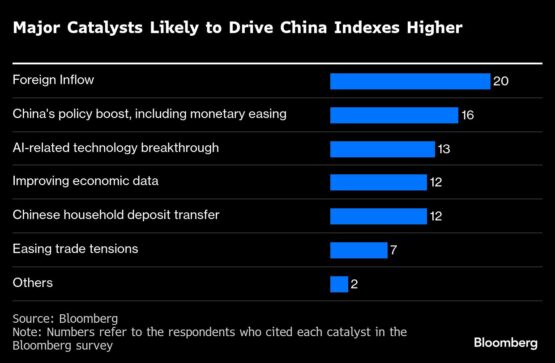

A reassessment of China’s technology sector, along with signals of increased foreign investment, has sparked optimism for a continuing upward trend. All but one of the 21 respondents in the survey identified foreign capital as a key factor for the next stage of the rally.

However, growing worries about inflated valuations are becoming evident, with 12 respondents indicating that AI is now the most crowded sector. “Every yuan allocated to AI capex boosts share prices, but in due time, investors will seek real cash flows rather than mere announcements,” Khurshid noted.

Policy Support

As the final quarter approaches, investors are seeking catalysts such as consumption during the Golden Week holiday, China’s Fourth Plenary Session, the Trump-Xi meeting at APEC, the Central Economic Work Conference in December, and any potential actions from the People’s Bank of China (PBOC).

Approximately half of the respondents believe that the PBOC will implement stimulus measures before year-end, citing the potential impact of a Federal Reserve rate cut to make room for further easing. However, Khurshid anticipates only modest actions from the central bank.

ADVERTISEMENT:

CONTINUE READING BELOW

“The PBOC has indicated its readiness to intervene should growth encounter further challenges,” he remarked. “I expect small, targeted measures rather than a broad stimulus initiative.”

The holiday and government discussions are unlikely to significantly shift the economic outlook in the short term, but announcements regarding policy changes could help restore market confidence, according to Meng Shen, director at the Beijing-based investment bank Chanson & Co. and a survey participant.

Sectors expected to benefit from the upcoming Fourth Plenary Session, scheduled for October, include AI, infrastructure, semiconductors, new energy vehicles, services, and real estate, based on participant insights.

Nonetheless, the realities of China’s economy may become evident next year. Short-term policy boosts may wane as full-year GDP data and other crucial metrics are released.

“Unless new topics arise to capture investor attention, market rationality may re-emerge,” Shen expressed.

© 2025 Bloomberg

Stay updated with Moneyweb’s comprehensive finance and business news on WhatsApp here.